Five Key Drivers of the "Discrepancy"

1. Loan Origination Fees: Timing is Everything

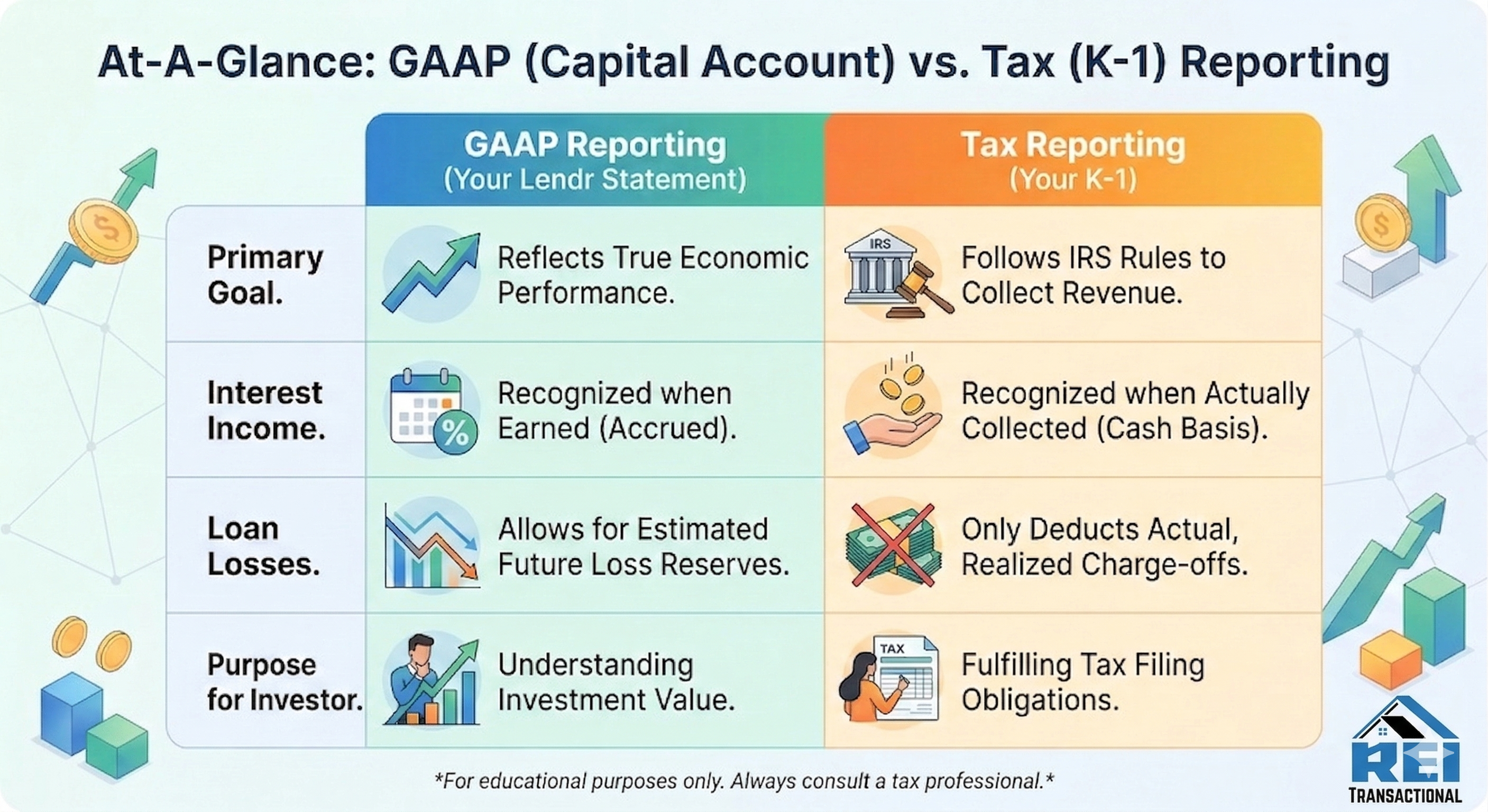

2. Interest Income: Accrued vs. Collected

3. Loan Losses: Looking Forward vs. Looking Back

Which Number Should I Focus On?

If you are looking for an accurate picture of the current value of your investment and how your capital is performing, refer to your Lendr Capital Account Statement. As we continue to grow, the gap between these two reporting methods may widen, but that is simply a byproduct of a scaling portfolio and complex tax code—not a reflection of diminishing returns.